Britain is facing a ticking timebomb over crippling debt according to a major study published today.

The Centre for Social Justice (CSJ) think tank says that the average household debt now stands at £54,000 – double the level a decade ago and despite record low interest rates.

There is a growing fear that the cost of living will force more and more people into crippling debt which they will not be able to repay, and ultimately leave thousands at risk of losing their home.

The CSJ was formed in 2004 by Iain Duncan-Smith but this latest study, called ‘Maxed Out’, ironically warned that two of the flagship policies Mr Duncan-Smith is implementing as Work and Pensions Secretary – the ‘bedroom tax’ and universal credit – could plunge more people into debt.

Although the CSJ backed the ‘principle’ of the ‘bedroom tax’ imposed on tenants in public housing, it said the ‘spare room subsidy’ should not have been removed unless those tenants had refused a ‘reasonable offer’ to ‘downsize’ or work longer hours.

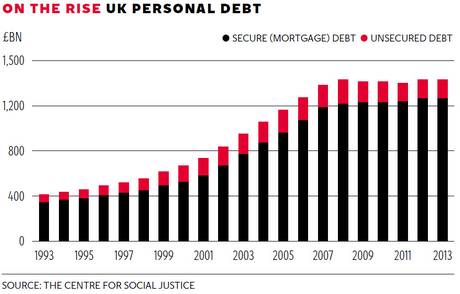

The study revealed that more than 5,000 people are already being made homeless each year because they cannot pay their mortgage or rent; personal debt in the UK now totals £1.43 trillion, close to its all-time high; and average household debt stands at £54,000 – almost twice the level a decade ago.

Although much of the debt stems from mortgages, the report warned that poor people were hit hardest as unsecured consumer debt has almost tripled in the last 20 years, to nearly £160 billion.

According to the CSJ, households owe the equivalent of 94 per cent of the UK’s economic output last year.

Only Ireland has a higher ratio of personal debt to GDP amongst European countries.

The CSJ said more than 26,000 UK households have been classed as ‘homeless’ by local authorities in the past five years, and warned that the number could increase if interest rates rises. Almost four million families do not have enough savings to cover their rent or mortgage for more than a month.

Another timebomb is the number of people retiring before they have paid off their mortgage. About 40,000 interest-only mortgages are due to mature each year between 2017 and 2032 where the householder will be over 65.

Between now and 2020, a third of the shortfalls on endowment mortgages will amount to more than £50,000.

Although the CSJ backed the principle of the “bedroom tax” imposed on tenants in public housing, it said the ‘spare room subsidy’ should not have been removed unless they had refused a ‘reasonable offer’ to “downsize” or work longer hours.

Christian Guy, the CSJ’s director, said problem debt has ‘taken root in the mainstream of British society’.

He added: “Years of increased borrowing, rising living costs and struggling to save has forced many families into a debt trap that is proving very difficult to escape. Some of the poorest people in Britain are cut off from mainstream banking and have no choice now but to turn to loan sharks and high-cost lenders.”

The ‘Maxed Out’ study also showed that payday lenders have grown their business from £900m in 2008-09 to more than £2bn today.